How to calculate the amount of pension in a year. Calculation of old-age labor pension. Can I now count on a preferential pension? If yes, how to calculate it?

Since 2015, pension calculations in Russian Federation is being done in a new way. Now the size of the pension and the right to it depend on the number of points. Let's take a closer look.

What does a pension consist of?

The insurance pension (formerly called labor pension) is calculated according to the formula:

number of points * cost of one point.

The cost changes annually and is approved by Government Decree. Right to pension provision Those citizens who have earned at least thirty points during their working life have. Overall size pensions include an insurance part and a fixed payment (previously the base part). The size of the fixed payment is also approved at the state level.

That is, only points need to be calculated. And their number depends on the salary.

Conversion of pension rights acquired before 2002

- experience until 2002;

- average monthly earnings (taken from 2000-2001 or any 60 months before 2002);

- experience until 1991

The first indicator is taken into account in the form of an experience coefficient. It cannot exceed 0.75.

- The man began labor activity since January 1976. Total experience – 26 years. The seniority coefficient is 0.55 + 0.01 * (26-25), or 0.56.

- For a woman under the same conditions, the calculation looks like this: 0.55 + 0.01 * (26-20), or 0.61.

- If the work experience is less than 20 years (for women) or 25 years (for men), then the length of service coefficient is 0.55.

The calculation of average earnings for a pension is made through the “earnings ratio”. This is the ratio of the average monthly salary of a citizen to the average monthly salary in the state for the same time period.

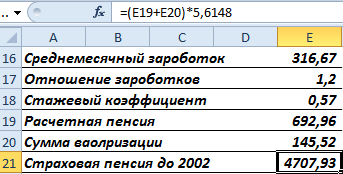

The citizen submitted to the Pension Fund a salary certificate for 60 months from 05/01/1986 to 04/30/1991.

Average earnings when calculating a pension are calculated using the formula:

The average monthly salary in the country is 230.1.

Earnings ratio: 1.2. The law established the maximum threshold for this coefficient: 1.2. Therefore, when assessing pension rights, not 1.38, but 1.2 is taken into account.

How to determine the size of a pension based on average earnings (earnings ratio):

- The estimated pension for citizens with a length of service coefficient over 0.55 is calculated as the product of the length of service coefficient, the average monthly salary coefficient and 1671 rubles. If the resulting value is less than 660 rubles, then you need to subtract 450 rubles. The amount of 1671 rubles is the SWP - the average monthly salary in Russia for the period 07/01/01-09/30/01 (constant value);

- If the length of service coefficient is 0.55, then a formula of the form is applied: (0.55 * average monthly salary coefficient * 1671 - 450) * (experience until 2002 / 25). This is for men. For women, the second multiplier is (experience until 2002/20). If the calculated value turns out to be less than 660 rubles, then for men - 210 * (experience until 2002/25), for women - 210 * (experience until 2002/20).

The woman retired in 2015. Total experience – 35 years. Until 2002 – 22 years. This is more than twenty years. This means that the formula for calculating the experience coefficient is as follows:

Let's assume the earnings ratio is 1.2. Since the length of service coefficient is greater than 0.55, the formula for the calculated pension looks like this:

The woman got a job in 1980. Consequently, she has work experience until 1991. When taking into account valorization, it will be necessary to add 10% to the calculated pension and 1% for each full year of work until 1991.

She worked for 11 years from 1980 to 1991.

Pension capital is indexed annually. As of December 31, 2014, the index value was 5.6148. Let's find pension rights in rubles for the period before 2002, taking into account bonuses and indexation:

Let's convert it into points. To do this you need to divide by 64.1.

This is part of a citizen's pension rights until 2002. When calculating a pension, the number of points will be multiplied by the value of 1 point accepted on the calculation date.

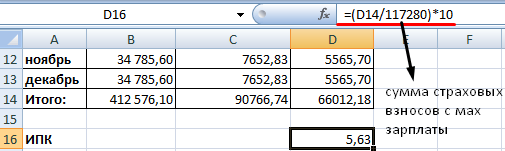

Calculation of the IPC for the period from 2002 to 2015.

- It is necessary to find the amount of transferred insurance premiums for a given period.

- Calculated insurance part labor pension as of December 31, 2014: amount of contributions / 228 (survival period).

- We find the IPK: insurance part / 64.1.

In other words: the insurance part of the labor pension is a pension calculated according to the “old” rules “minus” savings part and a fixed surcharge (set by the state).

Pension points since 2015

Calculated for each year length of service. For the calculation, the salary is taken, on which insurance premiums. Contributions to the FS – 22%. 16% goes to the formation of the insurance (10%) and funded (6%) part of the old-age labor pension. Let's assume that a citizen does not want to form a funded part separately.

To find the number of points earned in 2015, you need to:

IPK for different periods are added up and multiplied by the value of the point accepted on the date of retirement.

This is a simplified calculation without taking into account increasing factors, interrupted service, etc.

In short, the pension will depend on three factors: salary, length of service and the age when the person retires. The greater each of these components, the higher the future pension.

The most important change is that the insurance part of the pension will be calculated not in absolute numbers (that is, in accumulated rubles), but in points. Upon retirement, the number of points accumulated will be multiplied by their value. The latter is approved by the government and will be indexed to the level of inflation every year.

For example, in 2019 the cost of a point will be fixed at 87.24 rubles. At the same time, to count on insurance pension, you need to earn a certain number of points. For those who will retire in 2019, this is 16.2 points. But this figure will grow every year. And by 2025 it should be 30 points.

Minimum experience 15 years

Requirements for minimum experience. Now, to be eligible for a retirement pension, it is enough to work only 10 years. Officials considered that this was very little, and raised the qualification to 15 years. Nevertheless, this qualification will be increased gradually - until 2024. For example, in 2019, 10 years of experience is enough to qualify for an insurance pension.

Official salary

The size of your official salary also plays an important role. If your employer pays large contributions to the Pension Fund for you, then you will have greater pension rights in the future. Therefore, the higher the salary, the better. The main thing is that it be official.

However, there is some limitation. Insurance premiums are paid in full for those employees who receive no more than 710 thousand rubles per year (almost 60 thousand rubles per month). Based on this amount, the number of points you can earn per year is calculated. Now the maximum figure is 7.9 points (by 2021 it will increase to 10 points). You can get them if you worked all year and received the maximum salary (60 thousand rubles or more). If your salary is lower, then you will receive fewer points.

Incremental coefficients

The government has raised the retirement age. Nominally, women will be able to retire at 60, and men at 65, this will happen gradually by 2028. Plus, benefits will remain for those who work in hazardous industries. However, we will be encouraged to work longer. There are additional coefficients in the formula. For example, if a person postpones retirement for five years, then the pension will be approximately one and a half times larger. If for 10 years - more than double.

New pension benefits

Various incentives have appeared. For example, for large families. Before this, young mothers only had a period of care for a maximum of two children - 1.5 years for each, that is, three years in total. According to the new bill, when calculating length of service, 4.5 years will be taken into account - 1.5 years of care for each of three children. Plus, military service will also count towards your length of service.

Why do we get paid a pension?

Let us remind you that all working Russians pay 30% of insurance premiums from their official salaries. Part of the funds goes to free medicine and other social projects. We save only 16% of this 30% for old age. And now this money is divided into two parts.

Insurance - 10% - is used to pay current pensioners. And the Pension Fund records what contribution each employee made to this common pot; the size of the pension will depend on this in the future. And the funded part - 6% - is transferred to individual accounts. This money is invested in securities through management companies - public and private, as well as through non-state pension funds (NPFs). A funded pension is formed only for those citizens who were born in 1967 and later.

However, in 2018 and 2019, no contributions are made to the funded portion. All the money goes to the insurance part, that is, to pay current pensioners. Plus, the Ministry of Labor recently announced that almost 20% of Russians are not in the pension insurance system. That is, they receive their salaries in envelopes. This means only one thing - these people will receive social pension, which is extremely small.

Pension calculator on the pension fund website

At the end of last year, the Russian Pension Fund created a unified database of all future pensioners. Every Russian now has his own personal account, where he can see how many points he has already earned. To check whether your employer has made contributions for you and see your pension future, you need to take four simple steps.

✔ Register on the State Services portal (gosuslugi.ru). If you're already there, skip straight to the next step.

✔ Visit the website Pension Fund, find the button “Personal account of the insured person”, enter your login and password (exactly the same as on “State Services”).

✔ See data about your length of service and accumulated pension points. If you worked for some period, and the employer did not calculate or pay insurance premiums, then you will immediately discover this. In this case, you must immediately file a complaint with your employer. If he does not cooperate, then you should complain to the labor inspectorate. If you solve the problem without delay, you can quickly restore your rights.

✔ Use the calculator to understand how much pension you can earn in old age.

At the beginning of 2013, our state modernized the pension insurance system. The pension was divided into two parts. The first is cumulative and has not undergone any changes. The second is that the insurance company began to pay according to new formula.

The updated calculation method is based on a value such as , which is also called the pension point. It is accrued to every working citizen for every twelve months worked.

The pension score has a direct impact on the amount of future pension benefits. The greater the IPC value, the greater the amount the citizen will receive. It is worth taking a closer look at how to calculate your IPC for assigning an old-age pension.

What determines the value of the pension point?

In the process of calculating the size of one point, several parameters are taken into account. The main parameters influencing the size of the IPC value are the sum of points earned before and after 2015.

In addition, the increasing coefficient has a direct impact on the size of the IPC. Every year, the government of our state calculates the inflation rate in the country as a percentage. The resulting value is used when calculating the final value of the individual pension coefficient.

In 2017, the government determined the inflation rate - it was 3.2%. However, the multiplying factor was increased to 3.7%. Thus, the cost of one pension point from 78 rubles 58 kopecks, after indexation, is equal to 81 rubles 49 kopecks.

IPC calculation formula

note

Self-employed citizens, unlike employees, are required to pay their own contributions to the Pension Fund. So, if the annual income of an individual entrepreneur is less than 300,000 rubles, then the amount to be paid is 26,545 rubles. If more, then another 1% is added on the amount over 300,000 rubles. More about pensions individual entrepreneurs read in

During the entire period of a citizen’s official work activity, points are added to his pension account. The amount of pension capital accumulated before the 2015 reform is also converted into the described value.

In addition, there are exceptions. During certain moments pension points are credited to the citizen’s personal account even if he did not work. This occurs in the following situations:

- when a citizen is on leave to care for a child, until he reaches the age of one and a half years;

- undergoes military service in the army;

- is on leave to care for an incapacitated citizen.

According to paragraph 9, article 18 of the federal law, the size of the individual pension coefficient for the period of official work activity is calculated using the following formula:

IPK = (IPKs + IPKn) * KvSP

- IPC – the total number of points on the day the pension was assigned.

- IPKs – the number of points earned before January 1, 2015 (calculated by converting pension capital).

- IPKn – the number of points accumulated since January 1, 2015.

- KvSP – applied coefficient for increasing the IPC.

Calculation example

IPKi = (CVyear,i / NSVyear,i) * 10

- IPi – the number of points accumulated over the past year.

- СВyear,i – the amount of insurance premiums paid for the year.

- NSVyear,i – the amount of insurance premiums taken from the maximum contribution base.

Let’s say a citizen receives an official salary in hand in the amount of thirty thousand rubles. If the amount deducted as income tax is returned, then his formal salary is (income tax rate is 13%):

30,000 / 0.87 = 34,482 rubles

According to the formula, the resulting amount is multiplied by 12 to obtain the annual salary:

34,482 * 12 = 413,784 rubles

According to 2018 data, the maximum possible size of the contribution base is 1,021,000 rubles. Accordingly, the number of points that a citizen will earn, provided that he does not send payments directed to the funded part of the pension, respectively, all 16 percent goes to the formation of the insurance part, will be:

(413784 * 0.16) / (1021000 * 0.16) * 10 = 4.05 pension points

Where can you calculate your individual pension coefficient?

In order for a pensioner to find out his IPC, it is necessary to use a specialized calculator on the official Internet portal of the Pension Fund of the Russian Federation.

To do this, just visit the website, open the calculator and enter the following data:

- citizen's gender;

- year of birth;

- duration of compulsory military service;

- number of children (including planned ones);

- the period during which he plans to be on leave to care for children (including planned ones);

- the period during which he plans to care for incapacitated persons;

- expected length of official work experience;

- the size of the formal salary (before personal income tax).

After all the data has been specified, you need to click the “calculate” button. The system will automatically calculate the amount of future pension benefits.

Where can you get information about the values of IPKs and IPKn

You can obtain information about the number of pension points available in several ways:

- using the state Internet portal State Services;

- order a personal account statement on the PRF website;

- personally order a certificate by visiting Pension Fund branches at the place of residence.

Thus, pension points have a direct impact on the size of future pension benefits for citizens of our state. The calculation procedure is quite complicated, so to obtain information about the size future pension It is worth using specialized resources. This will avoid errors and inaccuracies in the calculation process.

Ask questions in the comments to the article and get expert advice

Every Russian needs to know what parts his pension will consist of upon reaching his cherished anniversary, after which he will no longer be able to work in old age.

Every year the retirement age approaches and therefore such information is increasingly of interest to every worker.

The complex procedure for calculating the amount of old-age benefits in the Pension Fund of the Russian Federation is incomprehensible to many employees. In addition, it is constantly changing due to the ongoing economic crisis.

In this article you can learn about the current procedure for calculating an old-age pension.

Legal regulation of the issue

In old age, a person loses the ability to work, which gives him the opportunity to receive income for living, therefore any legal state provides for elderly people social benefits. In the Russian Federation, there is an age of citizens approved in the legislation of the country, having reached which they can count on receiving an old-age pension.

The amount of benefits paid is individual for everyone, because... by its size influenced by many factors:

Russian legislation adopted a number of regulations that relate to the appointment state benefit by old age. These include the following laws:

- Federal Law No. 166 of December 15, 2001 “On pension provision...” with all amendments and additions.

- Federal Law No. 400 of December 28, 2013 “On insurance pensions”

- Federal Law No. 385 of December 29, 2015 “On the suspension of certain provisions of legislative acts of the Russian Federation, amendments to certain legislative acts of the Russian Federation and the specifics of increasing the insurance pension, fixed payment to the insurance pension and social pensions.”

IN this moment There is an intensive reform of pension provision for the older generation, so new regulations may be adopted that will supplement or repeal existing legislation.

Latest changes in this matter

Significant changes to the provision procedure social benefits in connection with retirement came into force at the beginning of 2015.

Now the insurance and savings share in the payment amount is supposed to be calculated not in banknotes, but in points (coefficients). In the future, when the payment deadline arrives, the amount will be calculated based on the number of points obtained as a result of the calculations and their value.

Now the insurance and savings share in the payment amount is supposed to be calculated not in banknotes, but in points (coefficients). In the future, when the payment deadline arrives, the amount will be calculated based on the number of points obtained as a result of the calculations and their value.

The government approved this procedure in order to more effectively protect pensioners from economic crises and inflation. At the time of reaching the age specified in the law, the solvency of the ruble drops significantly. And today its value, after some time, will be different in relation to the existing value at the time of making contributions.

When the value is reflected in points on the worker's individual account and then multiplied by their value, the state will be able to fulfill its obligations. Even if the labor pension is lower, an appropriate additional payment will be allocated to the benefit to achieve its size. In addition, there is an increase social assistance thanks to the annual

Adjustments to the payment of insurance benefits will be made automatically without an application from the pensioner. Only the amount of contributions paid by the employer for an employed pensioner has a direct impact on the amount of the additional payment, in contrast to the usual indexation, which is recalculated purely individually.

Adjustments to the payment of insurance benefits will be made automatically without an application from the pensioner. Only the amount of contributions paid by the employer for an employed pensioner has a direct impact on the amount of the additional payment, in contrast to the usual indexation, which is recalculated purely individually.

The Pension Fund of the Russian Federation annually, from August 1, recalculates benefits without an additional application from the pensioner on the basis of clause 3, part 2, art. 18 No. 400-FZ “On insurance pensions” dated December 28, 2013

Who is entitled to an old-age pension and at what age?

Every person, with age, gradually loses the ability to work and he needs financial support from the state to meet his own needs. In turn, at the legislative level it is approved age, upon reaching which workers become entitled to a pension.

For 2018 for Russians it is indicated within the following limits:

For 2018 for Russians it is indicated within the following limits:

- for men – 65 years;

- for women – 63 years.

There are exceptional cases that give right to retire and beyond different ages . Several factors can shorten the period:

- some categories of professions;

- conditions for fulfilling labor duties;

- territorial location of production where pensioners worked;

- birth of 5 or more children.

You can get advice from the Pension Fund about whether the work you are performing belongs to the preferential category for early receipt of social benefits.

In order to receive a full benefit upon reaching the age specified in the law, you must also have earned income. insurance experience, designated in the law “On Labor Pensions in the Russian Federation”. It is also different for men and women: 25 and 20 years old, respectively. In this case, only those years are accepted official work, for which contributions were made to the Pension Fund.

Are taken into account during the insurance period and non-working hours when the employee was on leave to care for:

A citizen’s total length of service also includes the period when he unemployment benefits were provided.

Today you can often find several names related to pensions:

- labor;

- insurance;

- cumulative.

For ordinary citizens, such definitions and which of them they need to count on in the future are not always clear. To understand this issue, let’s turn to the legislative framework.

Until the beginning of 2015, pension benefits were assigned in accordance with regulations dated December 17, 2001 N 173-FZ. It stated that old age labor pension was formed from two shares: insurance and savings. But two laws adopted in 2013 equated insurance and labor pensions. Thus, after the regulations come into force on January 1, 2015, workers of the Russian Federation who have earned an approved insurance period are paid an insurance pension.

Cumulative part may, at the discretion of the pensioner, be paid in a separate, independent payment.

Calculation procedure and amount of payments

The procedure for determining the amount that the Pension Fund will pay to a citizen in old age is set out in the following current regulations: N 400-FZ and N 424-FZ, which came into force on January 1, 2015.

Requirements updated to applicants for old age pension:

To calculate pension points, absolutely new formula.

To understand how pension benefits are calculated, you first need to understand terms legislation:

- Individual pension coefficient (IPK) or pension point (PB)- a value characterizing the amount of insurance premiums paid by the employer for the worker;

- Premium coefficient- an increasing parameter used to stimulate retirement from work at an older age;

- Fixed payment- the amount of the basic monthly amount of funds assigned by law to each citizen of the Russian Federation for a guaranteed payment in old age.

Herself formula for calculating insurance pension looks like that.

Ʃsp = Ʃpb * Cb 8 Pk1 + Ʃfv * Pk2,

- Ʃсп - the amount of funds calculated for the payment of old-age insurance pension;

- Ʃпб - pension points accumulated during work;

- CB - the price of 1 point established at the time of settlement;

- Pk1 and Pk2 - increasing bonus coefficients for retirement at a later period;

- Ʃfv - the amount of a fixed payment.

First, they calculate how much the employee has accumulated points during the deduction of insurance premiums in the PRF during his employment:

First, they calculate how much the employee has accumulated points during the deduction of insurance premiums in the PRF during his employment:

Ʃпб = Ʃtv / Ʃmax * 10,

- Ʃтв - the amount of funds paid according to the insurance tariff chosen by the employee;

- Ʃmax - the approved maximum contribution limit, withheld from earnings at a rate of 16%.

The first parameter, the amount of the contribution Ʃtv, is chosen by the enterprise employee independently, depending on how he wants distribute the collection:

- If only to an insurance account, then 16% of the contribution goes to the insurance fund.

- If you plan to form a funded part, then the insurance premium is reduced to 10%.

The calculations take into account only periods of official work when deductions and contributions to the Pension Fund were made from wages. This means that the salary received for work “in envelopes” will not affect the amount of monthly pension payments by old age.

Procedure for registering old-age pensions

An application for a pension should be addressed to the PRF branch located in the area of registration or residence of the applicant who has reached the established age.

An application form and relevant papers are filled out there.

It is better to prepare the attached package of documents. It includes the following sheets:

All copies must be confirmed as originals when submitting an application.

Features of accrual

It should be noted that the calculation of pensions is a purely individual matter. Some have earned “hot seniority”, some have not earned the required number of years, and some feel empowered and continue to work, having reached the approved years.

There are other nuances that significantly affect the size of the pension benefit.

For women and men

Many developed countries have set the same retirement age for both men and women. Russia is different from them.

The pension provision of the Russian Federation provides that the weaker sex has the right to more early date retirement. Difference in age and number of working years for total experience differs significantly depending on one gender or another.

The age and experience of the male part of the population are higher. This was described in more detail in the article above.

Early retirement

Due to certain circumstances, other persons may also qualify for early retirement benefits. These include:

- residents of the Far North;

- mothers of many children.

The law on insurance pensions contains a register of citizens of the Russian Federation who are given the opportunity to retire at an earlier age.

The innovations in the procedure for calculating pensions are described in the following video:

Since January 2015, another conversion of pension rights has taken place, now into pension points. For the first time since the Soviet period, the conversion of pension rights in Russia was carried out in 2002 - into pension capital.

From January 1, 2015, on the basis of laws No. 400-FZ and No. 424-FZ that came into force on December 28, 2013, the insurance and funded parts of the old-age pension became independent pensions.

We remind you that funded pension is formed and calculated according to the old principle (it still remains relevant only for citizens born in 1967 and younger), and the insurance pension is calculated according to the new formula - based on the pension points accumulated by the citizen during his working life.

SPS = FV × PC 1 + IPK × SPK × PC 2,

where SPS is the insurance pension.

FV - fixed payment.

PC 1 - bonus coefficient for increasing the fixed payment at a later retirement.

IPC - individual pension coefficient.

SPK is the value of the pension coefficient at the time of registration of the pension.

PC 2 - bonus coefficient for increasing the individual pension coefficient if a citizen continues to work despite the onset of retirement age or another condition for the emergence of the right to an insurance pension.

To understand how the old age pension is calculated according to the new formula, let’s consider what its main components are and how they are calculated: a fixed payment (the former basic part) and an individual pension coefficient, as well as who will be entitled to bonus coefficients.

So, we have become familiar with the general concepts regarding how to calculate a future pension. Now let's cover this topic in more detail.

Fixed part of the insurance pension

To calculate an old-age pension, you should know about the existence of a fixed payment (hereinafter referred to as FV) to the insurance pension established by Art. 16 Federal Law “On Insurance Pensions” No. 400-FZ dated December 28, 2013. In 2019, the payment amounted to RUB 5,334.19. This is the guaranteed minimum of the state for every Russian citizen of retirement age. The PV is indexed twice a year: on February 1, taking into account growth consumer prices and April 1 - at the expense of the Pension Fund's income for the previous period. April Fool's compensation is stated in the legislation as possible, and the possibility is determined by the Russian government.

Fixed payment to the insurance pension for various categories of citizens, northern pension

|

Gr-not entitled to ATP |

Number of dependents |

PV size (rub.) 1 |

|

Under 80 years of age and without a disability |

||

|

Those who have reached 80 years of age or disabled people of the 1st group |

||

|

Under 80 years of age and without disabilities, worked for Far North at least 15 years, insurance experience at least 20 and 25 years for women and men, respectively |

||

|

Those who have reached 80 years of age or are disabled in group 1, have worked in the Far North for at least 15 years, have an insurance record of at least 20 and 25 years for women and men, respectively |

||

|

Under 80 years of age and without a disability, have worked in the Far North for at least 20 years, insurance experience of at least 20 and 25 years for women and men, respectively |

||

|

Those who have reached 80 years of age or are disabled in group 1, have worked in the Far North for at least 20 years, have an insurance record of at least 20 and 25 years for women and men, respectively |

||

|

Work experience in agriculture at least 30 years old, not engaged in activities with mandatory pension insurance, live in rural areas 2 |

||

1 Amounts are rounded to hundredths of a ruble

Individual pension coefficient - the basis of the insurance pension

The individual pension coefficient (hereinafter referred to as IPC) is an innovation in the practice of calculating pensions. It has become a key component in the formula for a secure old age. One might even say - the basis for a citizen who wants to provide for himself after retirement and live with dignity. The higher the pensioner’s IPC, the greater the chance of achieving this goal.

The IPC is determined at the time of registration of an old-age pension and consists of the sum of the annual pension coefficients (hereinafter referred to as the APC) or pension points accrued to a citizen annually in the process of official work with a “white” salary. That is, for those years when employers transferred insurance premiums to the future pensioner.

New pension legislation also determined other periods for which citizens will be accrued pension points, and provided for coefficients for increasing the IPC and FV - for later registration of the implementation of pension rights.

How is the pension calculated in 2018-2019, are there any differences from the calculation in 2017

Now the formula for calculating the annual pension coefficient looks like this:

GPC = SSP / SSM × 10

Three quantities are involved in the calculation of the GPC:

Don't know your rights?

- The amount of insurance pension contributions from a citizen’s annual income (SSP).

- The amount of insurance premiums is 16% of the maximum contributory salary, established annually by resolutions of the Government of the Russian Federation (SSM).

- Multiplier 10. It was introduced for the convenience of calculating pension points. Also, 10 is the maximum number of annual pension points that can be awarded to a citizen in an accounting year.

But future pensioners will be able to receive 10 points per billing year only starting in 2021. And only those who do not participate in the formation of their funded pension.

Maximum values of the pension coefficient by year

|

Year of granting old-age pension |

Maximum value of IPC with contributions to funded pension |

Maximum IPC value without contributions to a funded pension |

1 When calculating pension coefficients, values are rounded to three decimal places.

When calculating an old-age pension, pension points for all years when the employee received insurance contributions from employers to the compulsory pension fund are summed up and an individual pension coefficient is displayed. The longer a citizen worked and the higher his salary, the higher his IPC will be. Accordingly, the higher the citizen’s IPC, the higher his pension income.

IPC= GPC 2015 + GPC 2016 +…GPC 2030

where GPC 2015 is the number of pension points earned by a citizen in 2015, GPC 2016 - in 2016, etc.

Calculation of individual coefficient: which years are better to take

Let's try to calculate our pension ourselves. As mentioned above, the annual pension coefficient is equal to the ratio of insurance pension contributions from a citizen’s income for the year to the maximum insurance pension contributions established by the state in the accounting year, multiplied by 10. For clarity, we will give examples. But first, let us recall that the total amount of pension insurance contributions paid by the employer to the employee is equal to 22% of his salary. Of them:

- 6% goes to the so-called solidary part of the Pension Fund, from which a fixed payment (basic part) of the insurance pension is paid to current pensioners;

- 16% are intended for the formation of the employee’s insurance pension or, at his request, 10% of them go to the insurance part, and 6% to the funded part.

An example of calculating the CPC with a deduction for an insurance pension of 16% of income

The salary of a citizen in 2018 is 20,000 rubles. per month. The amount of insurance contributions that the employer will pay to the Pension Fund will be equal to: 20,000 rubles. × 12 months × 16% = 38,400 rub.

In 2019, the maximum contributory salary is RUB 796,000. The amount of maximum insurance contributions from an employee’s income is RUB 127,360.

GPC = 38,400 / 127,360 × 10 = 3.015

The annual pension coefficient of a citizen in 2019 will be 3.015 pension points.

An example of calculating the CPC with a deduction for an insurance pension of 10% of income

For clarity, let’s take a citizen with the same wages for 2019. His employer contributes only 10% to the insurance pension, and the remaining 6% goes to the funded pension. The amount of pension contributions to a citizen’s insurance pension for the year will be: 20,000 rubles. × 12 months × 10% = 24,000 rub.

GPC = 24,000 / 127,360 × 10 = 1.884

The annual pension coefficient of a citizen in 2019 will be 1.884 pension points.

Since the size of future pensions directly depends on the value of the civil capital complex, it is clear from the examples that the formula for calculating pension points advocates refusal to participate in the formation of a funded pension.

Additional pension points: how to check the correctness of accrual

In addition to the pension points accrued to a working citizen for the payment of insurance pension contributions by his employer, when calculating the IPC, other periods during which pension contributions were not paid to the citizen are taken into account. For each full calendar year, the GPC is accrued under the following circumstances.

- Care of one parent for a child up to 1.5 years old (no more than 6 years in total):

- for the 1st - GPC = 1.8;

- for the 2nd - GPC = 3.6;

- for the 3rd or 4th - GPC = 5.4. - Caring for a disabled child, a group I disabled person, a person over 80 years old - GPC = 1.8.

- Military service by conscription - GPC = 1.8.

Point cost

The cost of 1 pension point in 2019 is 87.24 rubles. It will increase annually:

- February 1 in accordance with the inflation rate over the past year.

- April 1, according to a formula that includes such values as the amount of revenue to the Pension Fund budget in the form of insurance premiums and federal transfers.

Premium odds

Despite the fact that in Russia the retirement age comes much earlier than in most other countries of the world, Russian legislators have not taken the path of raising the age limit for eligibility for an old-age pension. But they included tools in the pension calculation formula that encourage people to retire later of their own free will.

If a citizen, having reached retirement age and the onset of pension rights, does not encroach on receiving funds from the Pension Fund, that is, does not apply for an insurance pension, but continues to work, the legislation provides for an increase coefficient of the fixed payment to the insurance pension (in our formula PC 1) and an increase coefficient individual pension coefficient (PC 2).

Indicators of bonus coefficients for full months of voluntary deferment of receiving a pension

|

Number of months |

IPC increase coefficient |

PV increase factor |

|

120 or more |

Based on the above indicators, it is easy to calculate that if a citizen does not apply for an insurance pension within 10 years after becoming entitled to it, then the PV will increase by 2.11, the IPC - by 2.32 times. And the old-age insurance pension will accordingly increase by almost 2.5 times.

Conversion of “old” pension rights into points

Citizens who reached retirement age in 2015 or who will reach it a few years later are worried about what will happen to their pension rights, which until now have been measured in rubles, and not in points. The same question worries people who are already receiving an old-age pension - after all, its further indexation will take place on the basis of pension points, which they do not seem to have.

The new pension legislation has provided a formula according to which pension rights formed before January 1, 2015 will also be converted into points:

PC = SCH/SPK

SCH - the insurance part of the labor pension as of December 31, 2014, excluding the basic and funded parts.

SPK is the value of the pension point at the time of retirement.

The resulting sum of points will either constitute the citizen’s individual pension coefficient if he is already a recipient of an insurance pension or is retiring, for example, in 2019, or will be added together with subsequent annual pension coefficients for the withdrawal of the IPC.

How pension is calculated examples

Let's return to the new pension formula:

SPS = FV × PC 1 + IPK × SPK × PC 2

Now we know how its components are calculated, and we can find out the approximate size of the future pension.

Example 1. Retirement upon reaching retirement age

Citizen Ivanova reaches retirement age in 2017. In 2015, her pension rights were converted to 70 pension points. For 2015-2017, Ivanova will earn another 5 points.

Citizen Ivanova was on maternity leave twice for 1 year to care for a child up to one and a half years old. For her first child she received 1.8 pension points, for her second - 3.6.

By adding up all the pension points, we obtain the IPC of citizen Ivanova at the time of the right to apply for an insurance pension - 80.4 points.

Let's pretend that minimum size the fixed payment (FB) to the insurance pension in 2017 will be equal to 5,000 rubles, and the cost of the pension point (SPK) will be 100 rubles. Citizen Ivanova has no reason to use bonus coefficients, so the formula for calculating her pension looks like this:

SPS = FV + IPK × SPK

We calculate the old-age insurance pension of citizen Ivanova:

5,000 rub. + 80.4 × 100 rub. = 13,040 rub.

Example 2. Retirement after the right to an insurance pension arises

Let's try to calculate the monthly income of a pensioner from the distant future. Let's consider the conditionally ideal accrual option decent pension according to the new formula. After all, as legislators assure us, all their efforts and reforms are aimed at achieving a decent standard of living Russian pensioner. So, let's dream according to the new formula.

Citizen Petrov began working in 2015 at the age of 17 years. After working for a year, he was drafted into the army and served for two years. Behind military service he was awarded 3.6 pension points.

Citizen Ivanov received a higher education by correspondence and worked without interruption insurance period before retirement age and 5 years after the right to an insurance pension arises. In total, over 48 years of insurance experience, he earned 400 pension points. Together with the “military” points, his IPC was 403.6 points.

Let us assume that by the time citizen Petrov retires in 2063, taking into account all possible indexations, the PV will be 20,000 rubles. But citizen Petrov worked in the Far North for 20 years, so his financial allowance has been increased by 30% and amounts to 26,000 rubles.

Petrov’s bonus coefficients for 5 years of voluntary pension deferment are: for a fixed payment - 1.27, for an individual pension coefficient - 1.34.

Let the cost of a pension point in 2063 be 600 rubles.

We calculate the old age pension of citizen Petrov, taking into account bonus coefficients:

26,000 rub. × 1.27 + 403.6 × 600 rub. × 1.34 = 324,527.42 rubles.

Of course, it is difficult to imagine what will happen to the ruble by 2063, but today it looks more than decent.

It must be said that the given calculation of the old-age pension according to the new formula is approximate. Not only in the second example, but also in the first. If you want to get more exact result- register on the website of the Russian Pension Fund. The Pension Fund already has all the information about the pension rights of officially working or working citizens that have been formed to date, namely the number of years and months of insurance experience and the number of pension points already earned. This information can be viewed in the personal account of the insured person. Enter in pension calculator additional information about the place of your current job and salary, and about other periods for which pension points are calculated. Click the “Calculate” button and you will find out the size of your pension. Plan a well-deserved rest based on the result obtained, if it suits you. Or, if possible, take steps to increase your future pension. Now you know how to do this.

Can I now count on a preferential pension? If yes, how to calculate it?

Does the new one suggest pension reform preferential pension provision is of concern to those who worked in hazardous industries, in education, medicine, etc. Yes, today preferential pensions have been preserved.

It is quite natural that such citizens are also interested in how to calculate preferential pension. Let’s say right away that you shouldn’t look for any special differences in the calculation of a preferential pension from the calculation of a regular one, since the same formula is taken as a basis, its size is directly dependent on the amount of accumulated points, which have been taken into account since 2015. Deductions are transferred to these into the compulsory pension insurance system, using the formula:

IPO/NPO x 10

IPO - the amount of individual pension contributions for the year,

NPO - the standard amount of pension contributions for the year.

However, it will be much easier not to do independent calculations, but to go to the Pension Fund website and use the pension calculator available there.